When you think about car insurance, you probably think about protecting others in the event you cause an accident. But what happens when someone else causes the accident—and doesn’t have enough insurance to cover your injuries or damages?

That’s where Uninsured/Underinsured Motorist coverage (UM/UIM) comes in.

If you live in Colorado, this coverage is not just a smart choice—it’s one of the most important protections you can carry.

What Is UM/UIM Coverage?

Uninsured Motorist (UM) coverage helps pay for your medical bills, lost wages, and other damages if you’re injured by a driver who has no auto insurance.

Underinsured Motorist (UIM) coverage steps in when the at-fault driver doesn’t have enough insurance to cover the full extent of your losses.

It’s essentially your insurance for the other driver’s lack of coverage—and it’s there to protect you.

Why Is It Important in Colorado?

Colorado law requires drivers to carry auto liability insurance, but not everyone follows the rules—or carries enough. Here’s why UM/UIM is so important here:

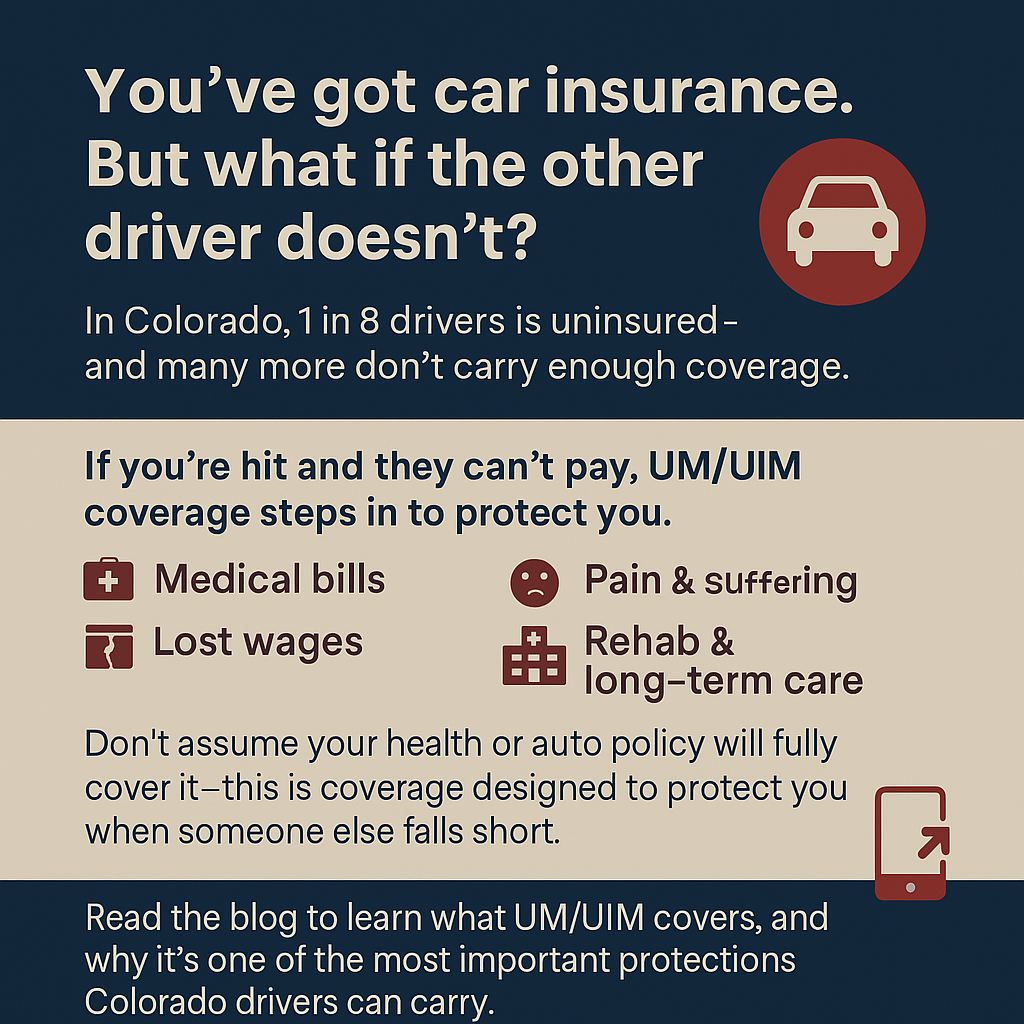

🚙 1 in 8 Drivers in Colorado Is Uninsured

Despite the law, many drivers on Colorado roads don’t carry any insurance. If one of them hits you, they can’t cover your injuries or lost income—UM coverage is what helps make you whole.

💵 Minimum Coverage Requirements Are Low

Colorado’s required liability limits are just $25,000 per person / $50,000 per accident. That can be quickly exhausted in a serious accident. UIM coverage ensures you’re not left paying out-of-pocket.

🏔️ High Medical Costs + Severe Accidents

Between rising healthcare costs and the potential for severe injuries from highway, mountain, or winter driving accidents, having extra protection can make a huge financial difference.

“Shouldn’t My Health or Auto Insurance Cover My Injuries?”

Not entirely—and not in the same way.

While your health insurance may help with medical bills, it won’t cover lost wages, pain and suffering, or long-term rehab the way UM/UIM coverage can. You’d also still be responsible for deductibles, co-pays, and out-of-network fees.

And your own auto-liability insurance only pays for damage or injuries you cause—not for your own medical needs when someone else is at fault.

UM/UIM coverage is designed specifically to protect you and your passengers when the person who hits you has little or no coverage. It can be a crucial financial safety net.

What Does UM/UIM Cover?

UM/UIM can help pay for:

- 🚑 Medical bills

- 💼 Lost wages

- 😕 Pain and suffering

- 🏠 Long-term care or rehabilitation

- 👨👩👧👦 Death benefits for family members (in fatal crashes)

It may also extend to passengers in your car, and sometimes even to you as a pedestrian or cyclist hit by a car.

Is UM/UIM Required in Colorado?

No—but it’s strongly encouraged.

By Colorado law, UM/UIM coverage must be offered when you buy an auto policy. If you decline it, you must do so in writing. That’s how seriously the state takes this coverage—it’s not mandatory, but it must be actively rejected.

Why You Shouldn’t Skip It

Too often, drivers focus on protecting others—but don’t think about protecting themselves. UM/UIM coverage is one of the most affordable ways to make sure you and your loved ones are financially protected if something happens.

If you’re injured by someone who can’t cover the damage they caused, this coverage could be the difference between recovery and financial strain.

Final Thought

Driving without UM/UIM coverage in Colorado is a gamble—and one that could cost you dearly.

Our team can walk you through your policy, explain your current limits, and help you decide what level of protection is right for your needs and budget.

Not sure if you have UM/UIM coverage?

We’ll check for you—just reach out.