How to stay compliant, reduce risk, and support employees during coverage transitions

When an employee leaves your organization or experiences a reduction in hours, health insurance doesn’t have to end immediately. That’s where COBRA comes in—but for many Colorado employers, the rules, timelines, and responsibilities can feel overwhelming.

Understanding how COBRA works (and when it applies) is essential—not just for compliance, but for protecting your business and supporting your people during transitions.

Here’s what Colorado employers need to know about COBRA in 2026.

What Is COBRA?

COBRA stands for the Consolidated Omnibus Budget Reconciliation Act, a federal law that allows eligible employees and their dependents to temporarily continue their group health insurance coverage after certain qualifying events.

Instead of losing coverage immediately, individuals can stay on your company’s health plan for a limited period—typically at their own expense.

Which Employers Are Required to Offer COBRA?

COBRA generally applies to:

- Employers with 20 or more employees

- Group health plans in the private sector and state/local government

If your organization meets this threshold, you are required to offer COBRA continuation coverage when a qualifying event occurs.

👉 Important:

If you have fewer than 20 employees, federal COBRA may not apply—but Colorado state continuation laws likely do (we’ll touch on that below).

What Qualifies an Employee for COBRA?

COBRA compliance is heavily dependent on timing. Missing a deadline can result in penalties and liability.

Here’s a simplified timeline:

- Voluntary or involuntary termination of employment (excluding gross misconduct)

- Reduction in hours

- Divorce or legal separation

- Death of the covered employee

- Loss of dependent status (e.g., aging off a plan)

Each of these events starts a strict timeline for employer responsibilities.

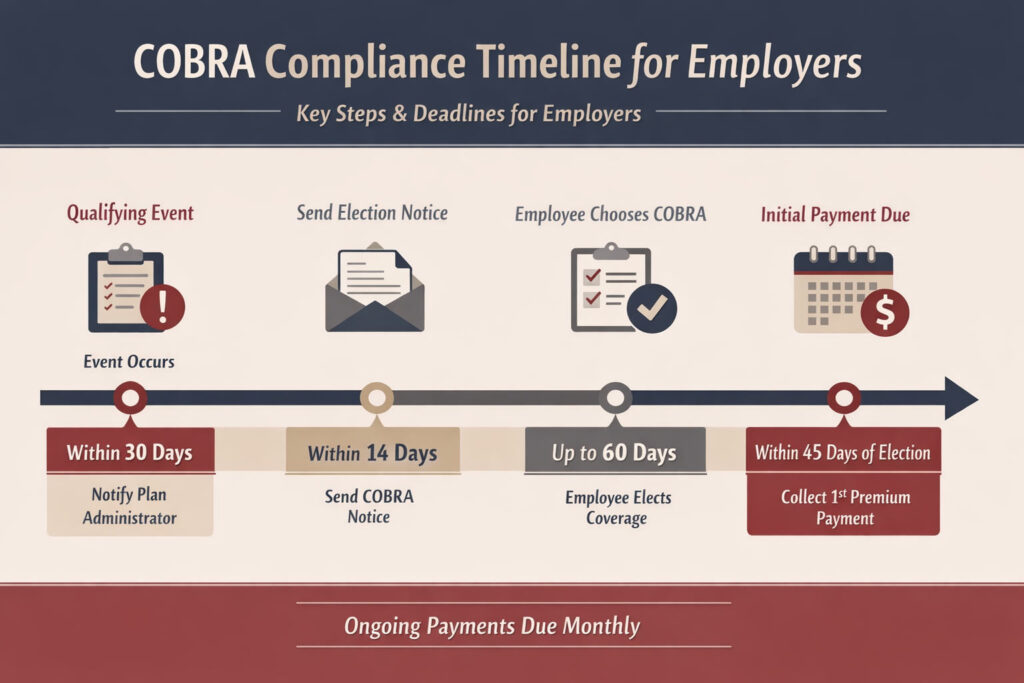

Key COBRA Deadlines Employers Must Know

COBRA compliance is heavily dependent on timing. Missing a deadline can result in penalties and liability.

Here’s a simplified timeline:

- Within 30 days: Employer must notify the plan administrator of the qualifying event

- Within 14 days after that: COBRA election notice must be sent to the employee

- 60 days: Employee has to elect COBRA coverage

- 45 days after election: Initial premium payment is due

These timelines are not flexible—accuracy and documentation matter.

How Much Does COBRA Cost?

Under COBRA, the employee typically pays:

- 100% of the premium, plus

- Up to a 2% administrative fee

That means individuals may pay up to 102% of the total cost of coverage.

Because employers often subsidize premiums during active employment, COBRA coverage can feel significantly more expensive to former employees.

How Long Does COBRA Coverage Last?

Coverage duration depends on the qualifying event:

- 18 months: Termination of employment or reduction in hours

- 36 months: Divorce, death of employee, or loss of dependent status

In some cases (such as disability), extensions may apply.

Colorado Employers: Don’t Overlook State Continuation Coverage

If your business has fewer than 20 employees, federal COBRA may not apply—but Colorado continuation coverage laws often do.

Key differences may include:

- Different eligibility requirements

- Varying coverage durations

- State-specific compliance obligations

Because these rules can be nuanced, it’s important to ensure your benefits strategy aligns with both federal and Colorado-specific requirements.

Common COBRA Mistakes (and How to Avoid Them)

Even well-run organizations can run into issues with COBRA. Some of the most common mistakes include:

- Missing notice deadlines

- Failing to properly track qualifying events

- Sending incomplete or incorrect election notices

- Miscalculating premiums

- Lack of documentation

These errors can lead to:

- IRS excise taxes

- Department of Labor penalties

- Potential legal exposure

A consistent, documented process is key.

Should You Outsource COBRA Administration?

Many employers choose to work with a third-party COBRA administrator—and for good reason.

COBRA administration involves:

- Tracking eligibility and qualifying events

- Managing strict timelines

- Sending compliant notices

- Collecting and tracking premium payments

- Maintaining documentation

Outsourcing can help:

- Reduce administrative burden

- Improve compliance accuracy

- Minimize risk

For growing organizations or lean HR teams, it’s often a worthwhile investment.

Final Thoughts: COBRA Is More Than a Compliance Requirement

COBRA isn’t just about checking a box—it’s about managing risk and supporting employees during important life transitions.

Handled well, it reflects:

- Operational discipline

- Care for your team

- A proactive approach to compliance

Handled poorly, it can create unnecessary exposure and frustration.

How Conexus Can Help

At Conexus Insurance, we help Colorado employers simplify complex benefits requirements—including COBRA and continuation coverage.

Whether you need:

- Guidance on compliance

- Help evaluating COBRA administration options

- Or a more streamlined benefits strategy

Our team is here to help you make confident, informed decisions.

Disclaimer

This content is for informational purposes only and is not intended as legal or tax advice. Employers should consult with legal counsel or a qualified professional regarding their specific situation and compliance obligations.