In a perfect world, your home insurance policy would always cover the full cost to rebuild your home after a disaster. But the reality? Construction costs don’t always stay the same—and a basic dwelling limit might not be enough. That’s where Extended Dwelling Coverage steps in.

If you own a home in Colorado, especially with rising rebuild costs in mountain towns, suburbs, and even the Front Range, extended dwelling coverage could be a critical part of your financial protection plan.

Let’s break down what it is, why it matters, and how it works.

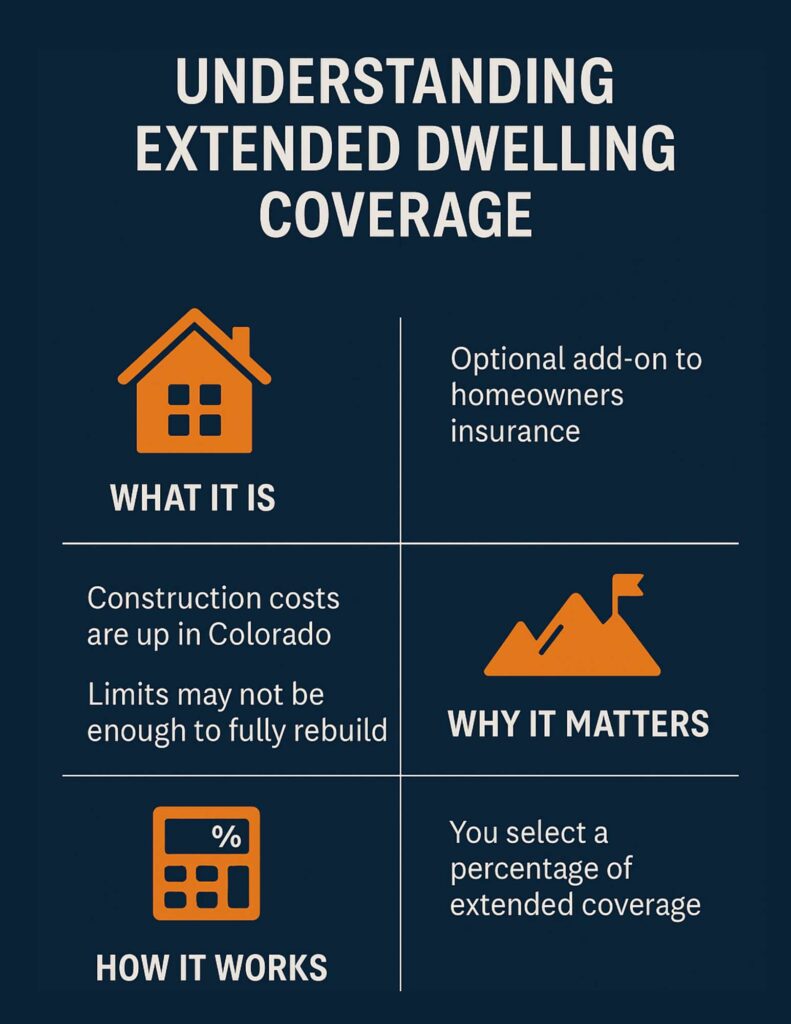

🔍 What Is Extended Dwelling Coverage?

Extended dwelling coverage is an optional add-on to your homeowners insurance policy. It provides additional coverage above your home’s insured dwelling limit (Coverage A) in case the cost to rebuild exceeds that amount due to inflation, demand surge after a wildfire or hailstorm, or miscalculations in reconstruction value.

For example, if your home is insured for $500,000 and you have 25% extended dwelling coverage, you’d have up to $625,000 available to rebuild if needed.

🏔 Why It’s Especially Important in Colorado

Colorado homeowners face unique risks that make extended dwelling coverage more than just a “nice-to-have”:

- Wildfires and hailstorms can lead to widespread property damage, which often drives up labor and materials costs fast.

- Labor shortages in mountain and rural areas can delay rebuilding timelines and increase costs.

- Rapid growth and inflation have pushed construction pricing up significantly across the state.

Even if your home was accurately valued when your policy started, those numbers might not hold up in a worst-case scenario.

✅ What to Look For in a Policy

Not all extended coverage endorsements are created equal. Here’s what to consider:

- Percentage of extension: Options typically range from 10% to 50% above your Coverage A limit. In Colorado, we often recommend at least 25–50% depending on location and home type.

- Guaranteed replacement cost: Some insurers offer this instead, which pays the full rebuild cost regardless of limit. It’s less common—but worth asking about.

- Regular valuation updates: Make sure your agent reviews your dwelling limit annually so the coverage grows with your home’s value.

A Smart Layer of Protection

Extended dwelling coverage isn’t about over-insuring—it’s about not falling short. If a covered loss happens, the last thing you want is to be out-of-pocket for tens (or hundreds) of thousands of dollars just to get back to where you started.

🤝 Let’s Make Sure You’re Covered for the Real World

At Conexus, we don’t just quote and forget. We walk through the “what-ifs,” clarify what your coverage actually protects, and help you make confident choices—without the insurance jargon.

If you’re not sure what your current policy includes—or if it’s keeping pace with today’s rebuild costs—we’re here to help you get clarity and confidence around your coverage.

Ready to review your dwelling coverage?

Let’s make sure your policy has the right guardrails in place to protect what matters most.