Especially important for Colorado contractors, vendors, and service providers

If you’ve ever been asked to provide a Certificate of Insurance (COI) before starting a job—or wondered whether you should be requesting one from a subcontractor—you’re not alone. COIs are one of the most common (and most misunderstood) tools in business insurance.

Whether you’re a contractor, vendor, property manager, or service provider in Colorado, understanding what a certificate of insurance does—and doesn’t—cover can protect your business and reduce risk in every project or partnership.

Let’s break it down.

✅ What Is a Certificate of Insurance?

A Certificate of Insurance (COI) is a one-page summary that proves your business has active insurance coverage. It includes key policy details like:

- Types of coverage (e.g., General Liability, Workers’ Compensation, Auto)

- Policy limits

- Policy effective and expiration dates

- Insurance company and producer information

- Named insured (that’s you or your company)

Think of it as your insurance “receipt”—a quick, standardized way to show other businesses that you’re covered.

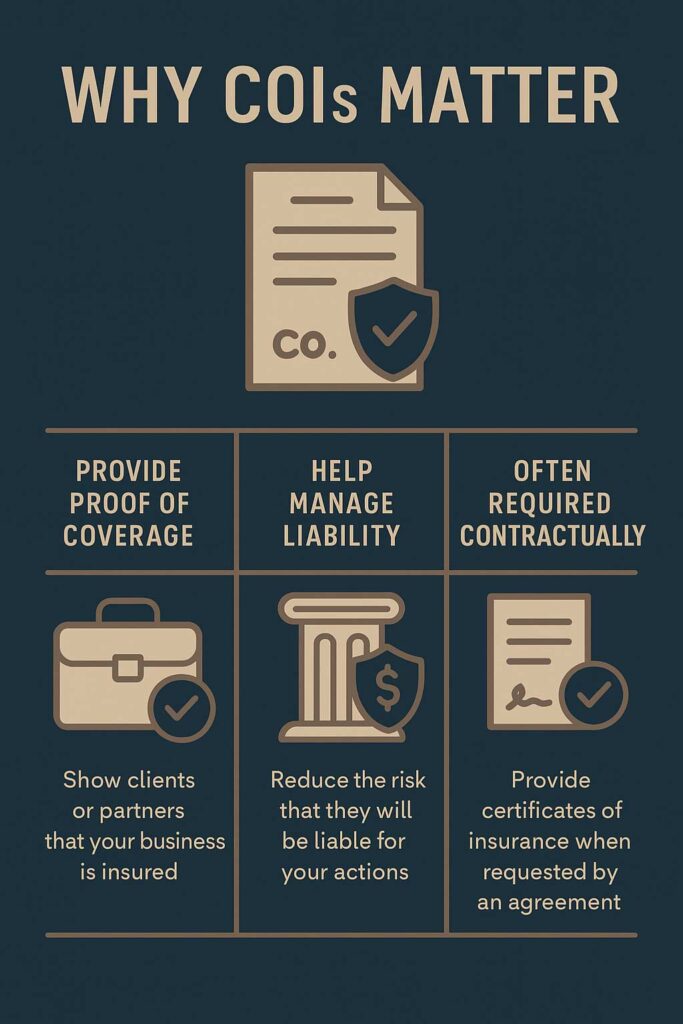

🧰 Why Are COIs So Important?

COIs are often required in business-to-business (B2B) relationships—especially in industries where one party’s work could create liability for another. This includes:

- Construction & contracting

- Property management

- Event vendors

- Commercial cleaning services

- Delivery and transportation companies

Here’s why COIs matter:

- They provide proof of coverage: A client, general contractor, or property owner wants to know that if something goes wrong, your policy—not theirs—will respond.

- They help manage liability: Without a COI, you might be exposing your business—or theirs—to claims that could have been avoided.

- They’re often a legal or contractual requirement: Many agreements require you to provide a COI before work begins. No COI = no job.

What a COI Doesn’t Do

Here’s where it gets tricky: A COI is not the policy itself. It doesn’t guarantee coverage, nor does it amend or extend the actual terms of the insurance. It’s simply a snapshot in time that confirms what policies are in place when the certificate is issued.

Also important: A COI doesn’t automatically make the certificate holder an additional insured—that requires a specific endorsement on the actual policy.

Best Practices for Colorado Businesses

If you’re issuing COIs:

- Keep them current: Make sure your insurance agent has the details for who needs to receive a certificate—and request one with each new contract.

- Understand what’s being shown: Know what limits, endorsements, and policy types are being shared.

If you’re collecting COIs:

- Verify the details: Make sure the name, coverage, and dates line up with your requirements.

- Ask about additional insured status: If you need to be named, that should be reflected in the policy—not just the COI.

- Track expiration dates: A COI is only valid for the policy term listed.

🤝 Need Help With COIs?

At Conexus, we work with business owners, contractors, and vendors across Colorado to make COIs easy to request, review, and manage. We help you stay compliant, protect your partnerships, and reduce the back-and-forth—so you can focus on the work, not the paperwork.

Need a certificate fast—or want to tighten your COI process?

Let’s connect. We’ll help make sure your certificates are working as hard as you are.