When employers design an employee benefits package, disability insurance is often one of the most misunderstood coverages. Many employees assume disability insurance only applies to catastrophic injuries, but the reality is that disabilities are more common than most people realize—and they can happen from illness, injury, or medical conditions that prevent someone from working.

Two common types of disability coverage offered through employer benefits programs are short-term disability insurance (STD) and long-term disability insurance (LTD). While both are designed to replace income if an employee is unable to work due to a disability, they serve different purposes and apply at different stages of a disability claim.

Understanding the difference between short-term and long-term disability insurance can help employers build stronger benefits packages and help employees better protect their financial well-being.

What Is Short-Term Disability Insurance?

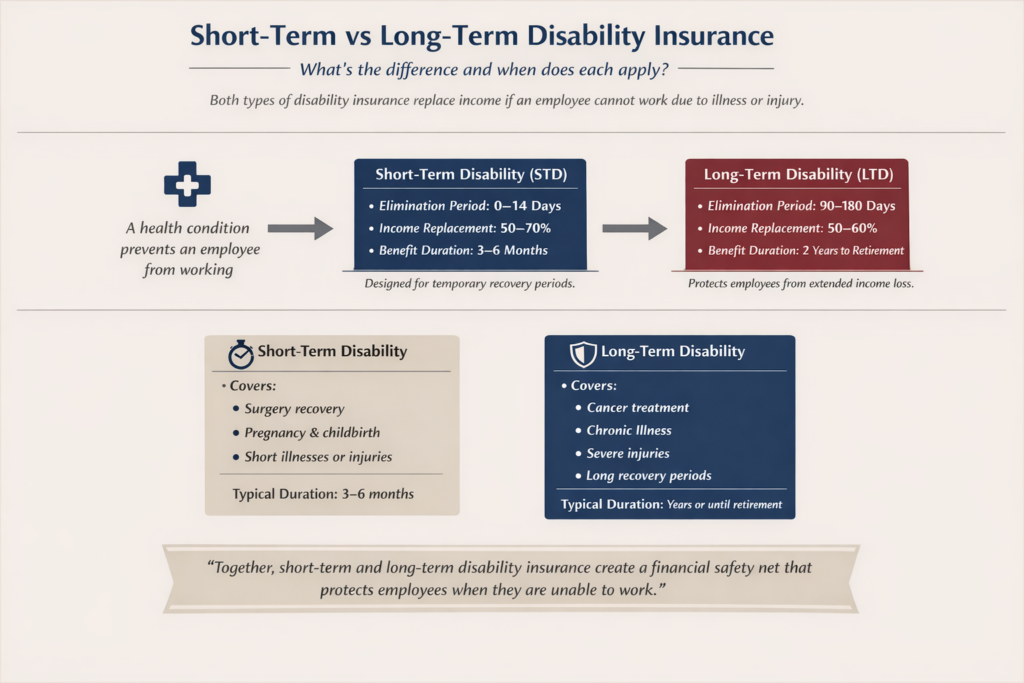

Short-term disability insurance provides temporary income replacement for employees who are unable to work due to a qualifying illness, injury, or medical condition.

This coverage is designed to support employees during shorter recovery periods, helping them maintain financial stability while they focus on getting better.

Common situations where short-term disability benefits may apply include:

- Surgery recovery

- Pregnancy and childbirth

- Non-work related injuries

- Serious illnesses that require time away from work

Short-term disability policies typically replace 50%–70% of an employee’s income, depending on the plan design.

Key Features of Short-Term Disability Insurance

Elimination period:

The elimination period is the waiting period before benefits begin. Short-term disability policies often have elimination periods of 0 to 14 days.

Benefit duration:

Benefits typically last 3 to 6 months, although some plans may extend up to 12 months.

Purpose:

Short-term disability provides income protection for temporary medical conditions or recovery periods.

What Is Long-Term Disability Insurance?

Long-term disability insurance provides income replacement when a disability prevents someone from working for an extended period of time.

While short-term disability covers the early stages of an illness or injury, long-term disability coverage protects employees if their condition lasts months or even years.

Long-term disability claims can arise from a wide range of conditions, including:

- Cancer treatment

- Heart disease or stroke

- Chronic illnesses

- Musculoskeletal injuries

- Severe mental health conditions

Because long-term disabilities can significantly impact financial security, this coverage plays a critical role in protecting employees and their families.

Key Features of Long-Term Disability Insurance

Elimination period:

Long-term disability policies typically have elimination periods of 90, 180, or 365 days.

This waiting period is often designed to begin after short-term disability benefits end, creating a continuous income protection strategy.

Benefit duration:

Benefits may last:

- 2 years

- 5 years

- 10 years

- To Social Security Normal Retirement Age

Income replacement:

Most long-term disability plans replace 50%–60% of income.

| Feature | Short-Term Disabilty | Long-Term Disabilty |

| Purpose | Covers temporary medical conditions | Covers extended or permanent disabilities |

| Elimination Period | Usually 0–14 days | Typically 90–365 days |

| Benefit Duration | 3–6 months | 2 years to retirement ages |

| Income Replacement | ~50–70% of income | ~50–60% of income |

| When It Begins | Shortly after disability occurs | After short-term benefits end |

In many employer benefits programs, short-term and long-term disability insurance work together to create continuous income protection.

How the Two Coverages Work Together

Think of disability insurance as a two-stage safety net.

- Short-term disability supports employees during the early phase of an illness or injury.

- Long-term disability provides protection if the condition lasts beyond the short-term benefit period.

For example:

- An employee undergoes surgery and needs 8 weeks to recover.

- Short-term disability replaces income during that recovery period.

- If complications extend the disability beyond several months, long-term disability coverage may begin once the elimination period is satisfied.

This coordination helps prevent gaps in income protection.

Why Disability Insurance Matters More Than Many Employees Realize

Many people focus on life insurance when thinking about financial protection, but disability insurance is just as important.

According to industry research, the average long-term disability claim lasts more than two years. Without income replacement, employees could face significant financial hardship.

Disability insurance helps employees continue paying for:

- Housing and mortgage payments

- Utilities and everyday expenses

- Healthcare costs

- Family financial responsibilities

For employers, offering disability coverage also supports employee well-being, retention, and financial security.

Designing the Right Disability Insurance Strategy

When employers evaluate disability coverage, several plan design elements should be considered:

- Elimination periods

- Income replacement percentages

- Benefit duration

- Employer-paid vs voluntary options

- Coordination with other benefits programs

Every organization’s workforce is different, which is why disability insurance should be thoughtfully integrated into the overall employee benefits strategy.

At Conexus Insurance Partners, we help employers evaluate disability coverage alongside the rest of their benefits program to ensure employees have meaningful protection when they need it most.

Final Thoughts

Both short-term and long-term disability insurance play an important role in protecting employees from income loss due to illness or injury.

Short-term disability helps employees recover from temporary medical conditions, while long-term disability provides financial protection if a disability lasts months or years. Together, they form a comprehensive safety net that supports employees during some of life’s most challenging moments.

Understanding the difference between these two coverages helps employers build stronger benefits programs—and helps employees feel more secure about their financial future.

Need Help Evaluating Disability Insurance for Your Team?

At Conexus Insurance Partners, we work with employers to design benefits strategies that support both organizational goals and employee well-being.

If you’d like help evaluating your disability insurance options or reviewing your current benefits program, our team would be happy to help.