In today’s increasingly litigious world, even a well-protected individual or business can face catastrophic financial loss if a serious claim exceeds the limits of standard insurance policies. That’s where umbrella insurance steps in.

Umbrella insurance provides an additional layer of liability coverage—typically starting at $1 million—that kicks in after the limits of your auto, homeowners, or general liability policies have been exhausted. Whether you’re a homeowner, high-net-worth individual, landlord, or business owner in Colorado, understanding the value of this protection could be critical to safeguarding your future.

What Is Umbrella Insurance?

Umbrella insurance is not a standalone policy, but a supplemental form of liability coverage. It doesn’t cover your own property; instead, it protects you from large claims or lawsuits where you’re found legally responsible for injury, property damage, or personal liability.

It provides:

- Extended liability coverage beyond the limits of home, auto, renters, or business liability policies.

- Coverage for certain claims not included in other policies (e.g., slander, libel, false arrest).

- Worldwide protection, not limited to incidents in Colorado or the U.S.

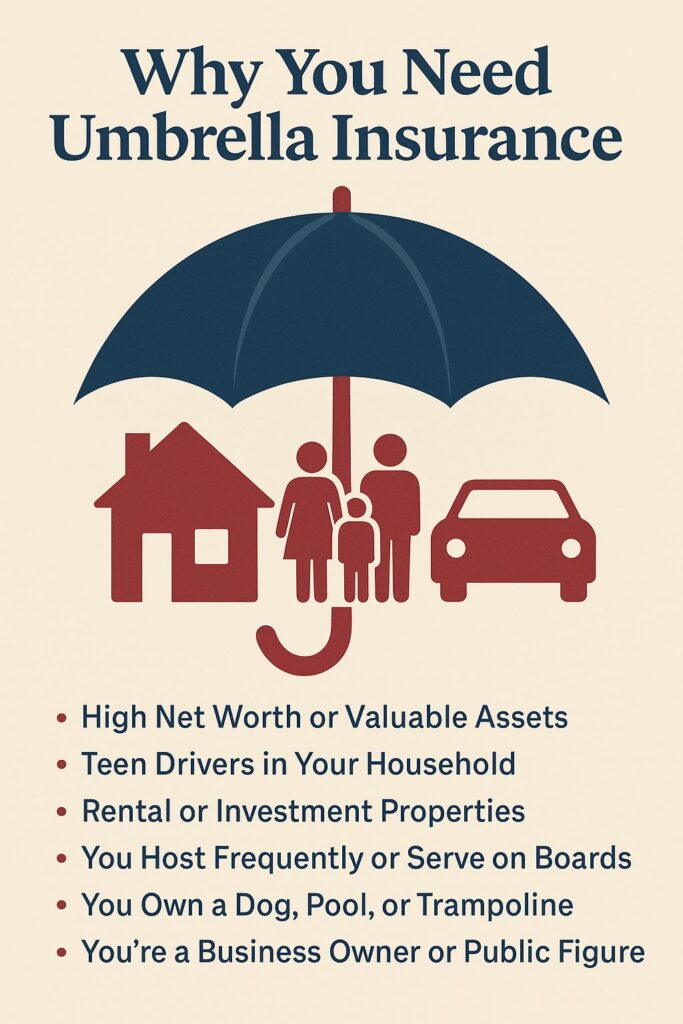

When Might You Need Umbrella Coverage?

- High Net Worth or Valuable Assets

If you have significant savings, a home with equity, or investments to protect, umbrella insurance ensures those assets aren’t wiped out by a large lawsuit or judgment.

- Teen Drivers in Your Household

Teen drivers are statistically more likely to be involved in serious accidents. If an auto accident they cause leads to injury or death, your basic liability limits may not be enough.

- Rental or Investment Properties

Landlords face exposure from tenant or guest injuries on their property. Umbrella coverage is a smart backup if legal damages exceed your landlord policy’s limits.

- You Host Frequently or Serve on Boards

If you entertain often, or serve on a nonprofit or HOA board, you could be held personally liable for injuries, alcohol-related incidents, or board-related decisions.

- You Own a Dog, Pool, or Trampoline

Attractive nuisances can increase your liability exposure. A serious dog bite or pool-related injury can easily exceed your homeowners coverage.

- You’re a Business Owner or Public Figure

Your public presence—or your business operations—can increase the likelihood of lawsuits. Umbrella policies add peace of mind and financial protection.

How Umbrella Insurance Works

Let’s say you’re involved in a car accident where you’re found liable for $1.5 million in damages, but your auto policy has a $500,000 liability limit. Without an umbrella policy, you’d be responsible for the remaining $1 million out of pocket. With a $1 million umbrella policy, those excess costs would be covered—protecting your home, savings, and income.

What Umbrella Insurance Does NOT Cover

To manage expectations, umbrella policies do not cover:

- Your own injuries or property damage

- Intentional or criminal acts

- Business activities (unless you have a commercial umbrella policy)

- Contracts you agree to (unless covered by underlying policies)

It also won’t cover professional errors—that’s what Errors & Omissions (E&O) or malpractice insurance is for.

How Much Does It Cost?

Umbrella coverage is relatively affordable given the large amount of protection it offers. Most $1 million umbrella policies start at $150–$300 per year, with each additional million costing less than the first.

Umbrella Insurance in Colorado: Local Considerations

Colorado’s growing population, active lifestyle, and evolving legal climate make it important to consider umbrella protection. Industries like real estate, construction, and transportation are especially vulnerable to high-stakes liability claims. But even families in Boulder or Westminster with teen drivers or Airbnb rentals face similar exposure.

Final Thoughts: Is Umbrella Insurance Worth It?

If you’ve ever wondered, “Could I afford to pay out-of-pocket for a $1 million+ lawsuit?”—umbrella insurance is your answer. It’s a safety net that protects what you’ve worked hard to build.

Whether you’re a Colorado homeowner, parent, landlord, or entrepreneur, an umbrella policy can provide peace of mind—and protection when you need it most.

✅ Need Help?

Not sure how much umbrella coverage is right for you? Contact a Conexus Insurance Advisor today to get a tailored risk assessment and quote.